Physical address

4 Merchant Place Corner Fredman Drive and Rivonia Road Sandton 2196

Postal address

PO Box 650149 Benmore 2010

The FNB Umbrella Funds Flexible option allows an employer to fully customise an employee benefits solution that suits both their needs and the needs of their employees.

Find out more

The FNB Umbrella Funds Bundled option provides a comprehensive pre-packaged solution which includes a pension or provident fund, life, disability and funeral cover.

Find out moreThe MarketStage strategy adjusts the risk profile based on market movements and years to retirement.

Money is invested in the FNB Growth Portfolio up until 7 years prior to retirement.

Members' fund credits are then allocated between the FNB Growth Portfolio to a more moderate/conservative portfolio (the Ashburton Stable Income Fund) 7 years prior to retirement, taking into account market circumstances as well as the member's time to retirement.

This MarketStage asset allocation between the Growth and Stable Income portfolios is reviewed regularly to maximise growth and minimise volatility and risk.

The Funeral Benefit pays a lump-sum benefit in the unfortunate event of the death of your employee, to their nominated beneficiary.

The pay-out can help to cover the immediate costs such as funeral and burial expenses.

The funeral benefit is a fixed rand amount per insured person, as selected by you, the employer, and pays out within 24 hours of receiving all required documents.

Depending on how you structure this benefit, your employee's spouse and up to 5 children may also be covered

The Life Cover Benefit pays out a lump-sum amount to the employee's beneficiary *, if the employee passes away.

The pay-out can help with providing financial support to dependants, settling outstanding debts, and to pay for children's education or settle estate duties.

The lump-sum amount is set by you, the employer, and expressed as a multiple of basic (or risk) salary, for example:

If an employee has an annual risk salary of R250 000 and you selected the life cover multiple as 2x annual risk salary, the employee's beneficiary will receive a lump-sum pay-out of R500 000.

* How you set up this benefit, determines if it pays out (as a lump sum or an annuity via a trust) to nominated beneficiaries directly, or to dependants / beneficiaries as per the Pension Funds Act.

We are able to offer your employees cover if they become permanently disabled and are unable to work. We offer two options of cover: a lump-sum pay-out or a monthly benefit if they suffer a disability.

The pay-out can help replace an employee's income, cover additional expenses, such as recuperation costs, pay off debt or pay for modifications to their home and car to accommodate for the disability or to cover monthly expenses, such as school fees, rent or home loan repayments.

Disability cover - protection against the cost of permanent disability

The Disability Benefit pays out a lump-sum amount to the employee if they become physically or (or mentally) impaired and if they are unable to earn an income due to permanent disability.

The lump-sum amount is set by you, the employer and expressed as a multiple of basic (or risk) salary. This may not exceed the life cover amount. For example:

If the employee has an annual risk salary of R250 000 and disability cover multiple is selected at 1.5x annual risk salary, the employee will receive a lump-sum pay-out of R375 000.

Income protection - protects your employees' livelihood

Income Protection pays a monthly benefit to the employee if they suffer a loss of income due to a disability, or if they become severely impaired. This benefit will be paid until the employee is no longer disabled or returns to work.

The monthly insured amount is set by you, the employer and expressed as a percentage of basic (or risk) salary. For example:

If the employee has an annual risk salary of R250 000 and the monthly disability income is selected at 75% of annual risk salary, the monthly disability income will be R15 625.

The Critical Illness Benefit pays out a lump-sum amount to your employee if they suffer from one of the specified illnesses or conditions.

The pay-out can help to cover additional expenses, such as recuperation costs, nursing or medical specialists, settling outstanding medical bills, and for 24/7 care.

The lump-sum amount is set by you, the employer and expressed as a multiple of basic (or risk) salary. For example:

If the employee has an annual risk salary of R250 000 and the critical illness cover multiple is selected at 1.0x annual risk salary, the employee will receive a lump-sum pay-out of R250 000.

Erika holds various legal qualifications and has served on the executive management of the Employee Benefits divisions of numerous long-term insurers and private fund administrators, mostly responsible for the legal and compliance departments. For the last 12 years she has been working as a legal consultant and fiduciary in the pensions field. She is a full member of the Pension Lawyers Association and has served as company secretary of a large pension fund administration company.

Erika has been appointed as an independent Trustee on various large privately administered funds in addition to serving as independent chairperson of the Board of Trustees of four large retail umbrella funds. She is currently the Principal Officer of the FirstRand Retirement Fund.

Her qualifications include a B Proc degree, Advanced Diploma in Labour Law, Higher Diploma in Pension Law, and the FAIS Regulatory Exam as a key individual.

Praneel is a Chartered Accountant by profession with over 20 years of banking experience, predominantly in a treasury environment. In that time, he fulfilled multiple roles beginning in finance before moving into strategic operations, portfolio management and Chief Risk Officer for Group ALM risks. He is currently the Head of Balance Sheet Management in the FirstRand Group.

Praneel has a passion for improving the retirement industry for the benefit of savers and is a Trustee on the FirstRand Retirement Fund (FRRF) and RMB Provident Fund (RMB PF), as well as chair of both the FRRF Investment Sub Committee and RMB PF Investment Sub Committee, having previously chaired the FRRF Audit and Risk Committee.

Praneel is a qualified CA (SA), and holds a BACC as well as a Postgraduate Diploma in Auditing.

Simon is a Registered Financial Planner (RFP) with more than 35 years' experience in the financial services sector, including long term insurance, stockbroking, investment management and financial advisory services. He holds the FSCA Regulatory Exams (RE) certificates; RE1: Key Individuals, RE3: Discretionary, and RE5: Representatives. He also has the FSCA Trustee Toolkit certificate and serves on some boards of management as an Independent Chairperson, and an Independent Trustee on others. He is a member of the Financial Planning Institute (FPI)..

He is one of the Founders of SM Mohapi Financial Services (Pty) Ltd, FSP722, T/A Mohapi Group, an accredited outfit by the FSCA as Investment Managers and Financial Advisors with a 20-year track record.

He is a graduate of the Stock Market College (SA), holds a Diploma in Investment Management (RAU), and a Graduate Diploma in Company Direction (NQF7) with the Institute of Directors (IoD) in collaboration with the Graduate Institute of Management & Technology (GIMT).

Mathias is a qualified Actuary with more than 15 years' experience working in the Employee Benefits sector. Over the past 15 years, he has worked at various long term insurers as a Consulting Actuary and Asset Consultant to some of the largest stand alone and umbrella retirement funds within the industry. Mathias is passionate about assisting retirement fund members to achieve favourable retirement outcomes through the management of the various retirement fund related risks associated with planning for retirement.

Mathias is a qualified Actuary (FASSA) and a holder of a BCom (Hons) degree in Actuarial Science. He is also an approved Valuator of both Defined Benefit and Defined Contribution Schemes, an approved Liquidator of retirement schemes and an approved Key Individual in terms of the FAIS Act.

As your trusted financial partner, FNB helps you select the best option for your business.

The Funds' primary aim is to protect and grow contributions to best enable members to meet their needs in retirement. The Funds offer a wide variety of investment portfolios, designed to meet the diverse needs of participating employers and their employees.

The Funds have a Trustee-choice Default Portfolio ('the default') and they also offer members investment choice, depending on the option selected by the employer. If the employer selected the Bundled Option, members can only be invested in the default, however if members are in the Flexible Option, they will have additional investments to choose from.

We pay a lump-sum benefit in the unfortunate event of the death of your employee, to their nominated beneficiary.

Read More

We offer your employees cover if they become permanently occupationally disabled and are unable to work.

Read More

We pay out a lump-sum amount to your employee if they suffer from one of the specified illnesses or conditions.

Read More

The FNB Umbrella Funds will be managed by a team of reputable industry

professionals that will guide and advise the fund every step of the way.

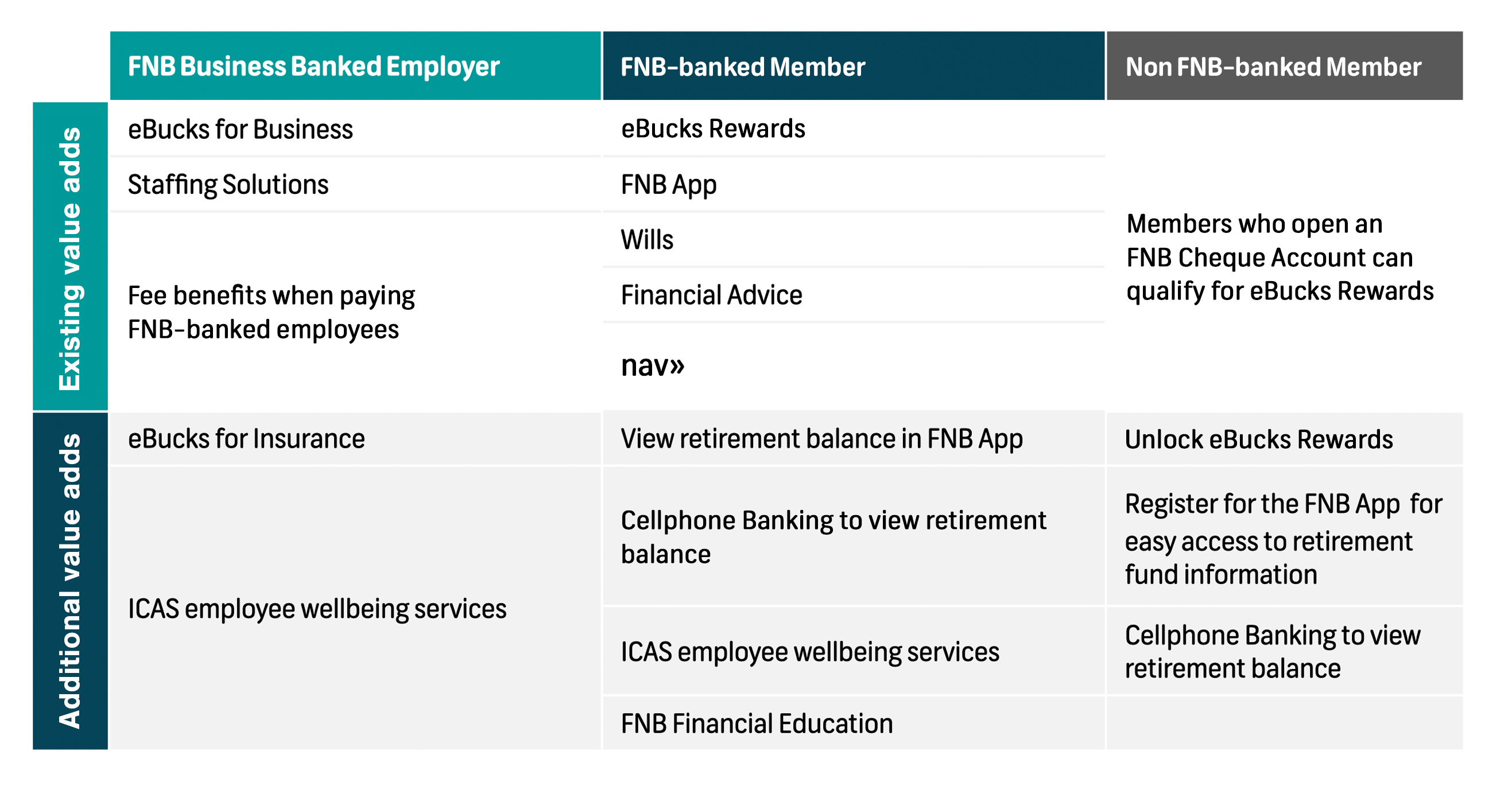

As an employer you get even more value from taking care of your employees. You can get a percentage of your annual Group Funeral premium back in eBucks.

Employees with a qualifying FNB account can get eBucks points every month for saving towards retirement.

eBucks terms, conditions and rules apply.

Your eBucks reward level will determine the percentage back in premiums.